In recent years the European Commission has compiled a legislative package that reforms the regulation of online commerce, among other things by extending one-stop shop systems. The majority of the directives and regulations that form part of the package will enter into force on 1 July 2021, and the rules implemented in the VAT law will also take effect from that date. Since the foundations of international e-commerce rules will change almost completely from 1 July, those affected should prepare for these significant changes well in advance. We would like to draw attention to the most important tax law changes affecting international e-commerce and distance selling.

Most important elements of the new regulation

The goal of the European Commission is to standardise and simplify the VAT rules that affect e-commerce. They basically want to make cross-border commerce easier, create a level playing field, and reduce the administrative burdens of businesses. The most important elements of the new regulation:

- expansion of the application of one-stop shop systems,

- transformation of the rules on product imports (import one-stop shop, termination of tax-exempt status for low-value imported packages, i.e. below EUR 22),

- inclusion of electronic platforms (intermediaries) in taxation in certain cases,

- change in definition of distance selling.

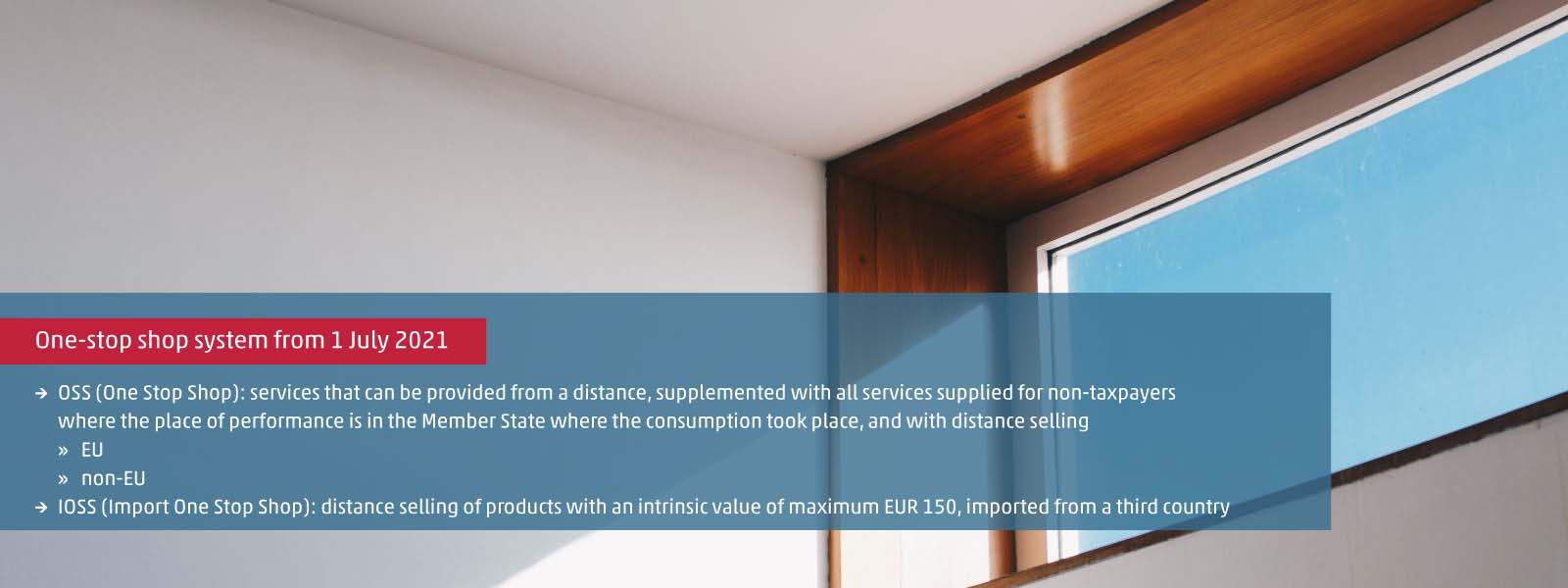

Wider application of one-stop shop systems

The one-stop shop system currently available is the so-called MOSS system (Mini One Stop Shop), which is only applicable for services that can be provided at a distance (telecommunications, electronic, radio and audiovisual services). From 1 July, the name of the MOSS system will change to OSS and its application will be extended with all the services provided for non-taxpayers where the place of performance is in the Member State where the consumption took place, and with distance selling. Within the OSS we can distinguish between EU and non-EU one-stop shop systems depending on which transactions these can be applied for. Additionally, a separate one-stop shop system will be created for the distance selling of products with an intrinsic value of no more than EUR 150, imported from a third country: the IOSS (Import One Stop Shop).

Common features of one-stop shop systems

Perhaps the most important common characteristic of all three one-stop shop systems is that selecting them is not mandatory, just an option. Businesses that use the one-stop shop systems can decrease their administrative costs significantly. The essence of these systems is that taxpayers fulfil their tax obligations affecting several Member States simultaneously by submitting one tax return in one specific Member State, thus sparing the need to register in the other Member States.

An additional common characteristic of one-stop shop systems is that there are no rights of deduction. Deductible taxes can basically be reclaimed through tax refunds. In certain cases, the given taxpayer may be registered in the Member State where the registration took place. In this case, the right to deduction can be applied in the tax return submitted in the given Member State.

Change in the rules of distance selling

The definition of distance selling will change as of 1 April, and from that time onwards there will be two types of distance selling: intra-Community distance selling and the distance selling of imported products.

The thresholds defined by the individual Member States will be cancelled, including the threshold of EUR 35,000 in the case of Hungary for example, while taxpayers using distance selling can register in the one-stop shop system and settle their tax liabilities in respect of several Member States simultaneously.

Let’s take an example. A company based in Hungary conducts distance selling from Hungary to several states of the EU (Germany, Austria, Slovakia). Based on the rules prior to 1 July, the company must monitor whether the value of its sales to the individual Member States exceeds the threshold in the given Member State (e.g. in the case of Germany it is EUR 100,000). If not, it can issue invoices with Hungarian VAT, but if the threshold is exceeded, it has to register in the given Member State. Based on the rules valid from 1 July, if the above Hungarian company selects the one-stop-shop system it must file its tax return and pay (via the return) the VAT on its sales to the other Member States (according to the VAT rates valid in the given Member State), thereby avoiding the need to register in the other Member States. It is important for the Hungarian company to report its sales with a place of performance in Hungary in VAT tax return no. 65, and not in the one-stop shop system.

Filing of tax returns

Tax returns must be filed electronically in each of the one-stop shop systems: quarterly in the EU and non-EU one-stop shop system, and monthly in the import one-stop shop system. The deadline for the tax returns and the payment of taxes is the last day of the month following the given tax assessment period.

Taxpayers registered in Hungary’s one-stop shop system should prepare their tax returns in HUF, while for conversions, the exchange rate published by the European Central Bank and valid on the last day of the tax assessment period should be applied.

Adjustment of tax returns

If the tax returns already submitted must be revised, taxpayers can do so in a subsequent tax return within three years of the filing deadline of the original tax return. Revisions are possible even after three years, but within the limitation period. Yet this is not done in the one-stop shop system, you should contact the competent tax authority in this matter.

Transitional rules

Taxpayers have the opportunity to register in one of the one-stop shop systems from 1 April 2021. Taxpayers already registered in the one-stop shop system as of 1 April 2021 because of services that can be provided from a distance do not have to register again. However, they should not forget to report some data to the national tax and customs authority by 15 June. But taxpayers already registered in the one-stop shop system and who now want to use it as a distance seller must register in the EU’s one-stop shop system.

Problem of online data reporting for invoices

In line with previous announcements, from 4 January 2021 the online invoice 3.0 system was launched in Hungary as the third and final step of extending online data reporting for invoices in Hungary. Upon the introduction of online invoice 3.0, the data reporting obligation for invoices is extended, among others, to include invoices issued to non-taxpayers, such as natural persons. While the VAT law exempts taxpayers registered in the one-stop shop system in Hungary from online invoice data reporting, this exemption is only valid from 1 July. Consequently, taxpayers who currently conduct distance selling and who wish to utilise the opportunities offered by the one-stop shop system from 1 July, would still have six months to fulfil their Hungarian online invoice data reporting obligation. Nevertheless, to be able to bridge this half-year period and gain exemption from the data reporting obligation, these taxpayers can utilise the moratorium until 30 June (that is originally in force until 31 March for other taxpayers), provided that they register in the one-stop shop system in their home country until 1 July and they make only distance selling to Hungary).

Although one-stop shop systems represent significant administrative easing for enterprises, it is obvious that companies involved in e-commerce should prepare for important changes from 1 July. It is worth starting to prepare in time. If your company is affected, please do not hesitate to contact our tax consulting team.