Efforts to digitalise tax systems are coming increasingly to the fore, not just in Hungary but also at EU level. One of the main objectives of VAT digitisation – and the digitalisation of other taxes – is to make it harder to conceal tax revenues and make it easier and more efficient for the tax authorities of Member States to collect them. Examples of this include tax administration measures optimised for the digital world, reciprocal and efficient exchange of information between Member States, or the simplification of tax administration by digital means.

One of the specific tools of VAT digitalisation, which we already covered in an earlier article is ViDA (VAT in the Digital Age), the European Commission’s package of proposals for digitalising certain aspects of the EU’s common VAT system. Although these are only proposals, it is worth preparing for them in advance so that taxpayers are not caught unawares by the digital switchover. Although in a different field, Hungarian legislators are also trying to prepare us for this because the e-VAT system became available from 1 January 2024, which aims to simplify the submission and validation of VAT returns.

E-invoicing

One of ViDA’s key objectives is to promote electronic invoicing in as many areas as possible. To this end, the concept of an e-invoice and the provisions on e-invoices will likely be amended in the Common VAT Directive (and then in the Hungarian VAT law). In some cases, use of e-invoices may become mandatory.

It could be useful for taxpayers to introduce e-invoicing before application becomes mandatory, but there may of course be other benefits to switching over: in many cases it is simpler, cheaper, requires less administration and fewer tools, and it is easy to automate. Although this is an area heavily regulated by law – in addition to the Act on VAT, the provisions of Ministry of Innovation and Technology (ITM) Decree No. 1/2018 (VI.29) on the rules of digital archiving must also be taken into account – the NAV published a very useful and comprehensive summary (available only in Hungarian here) in spring 2020 on the most important information regarding electronic invoices. This can be found on its website. The release of the summary was prompted by the coronavirus pandemic, so it is almost four years since it was first published, but its content is still valid today and it contains useful information that is worth revisiting after all this time. We believe the most interesting and useful details are as follows:

- An invoice that has been printed on paper, scanned and sent by email, for example as a PDF file, also qualifies as an electronic invoice. Of course, invoices issued, sent and received in this way must be stored in accordance with the requirements of the ITM Decree, i.e. compliance with the requirements of authenticity of origin and integrity of data must be ensured.

However, please note that it is not considered good practice for a printed invoice to be sent by email, reprinted by the recipient and kept on paper.

- The use of e-invoices also requires the consent of the invoice recipient, which, according to the NAV, doesn’t just mean formal acceptance, this can also happen via the tacit consent of the invoice recipient by paying the invoice.

- With regard to e-invoices, as mentioned in the first point, archiving in accordance with the ITM Decree must be ensured in such a way as to guarantee the authenticity of origin of the invoices, the integrity of their data content, and their legibility. These can be achieved with various digital tools, such as sending invoices via an EDI (Electronic Data Interchange) system or using qualified electronic signatures. It may be useful to know, however, that for sole traders or individual taxpayers, so-called AVDH (Azonosításra Visszavezetett Dokumentum Hitelesítés – Identification-Based Document Authentication), which is available free of charge to all those with government portal access in Hungary, may be an appropriate solution.

It is also accepted if the so-called hash code of an electronically issued invoice is entered into the online invoicing system and the parties save the e-invoice by preserving the hash code. In this case, no further action is required for the archiving since the hash code ensures the authenticity of the invoice and the integrity of its data.

E-VAT

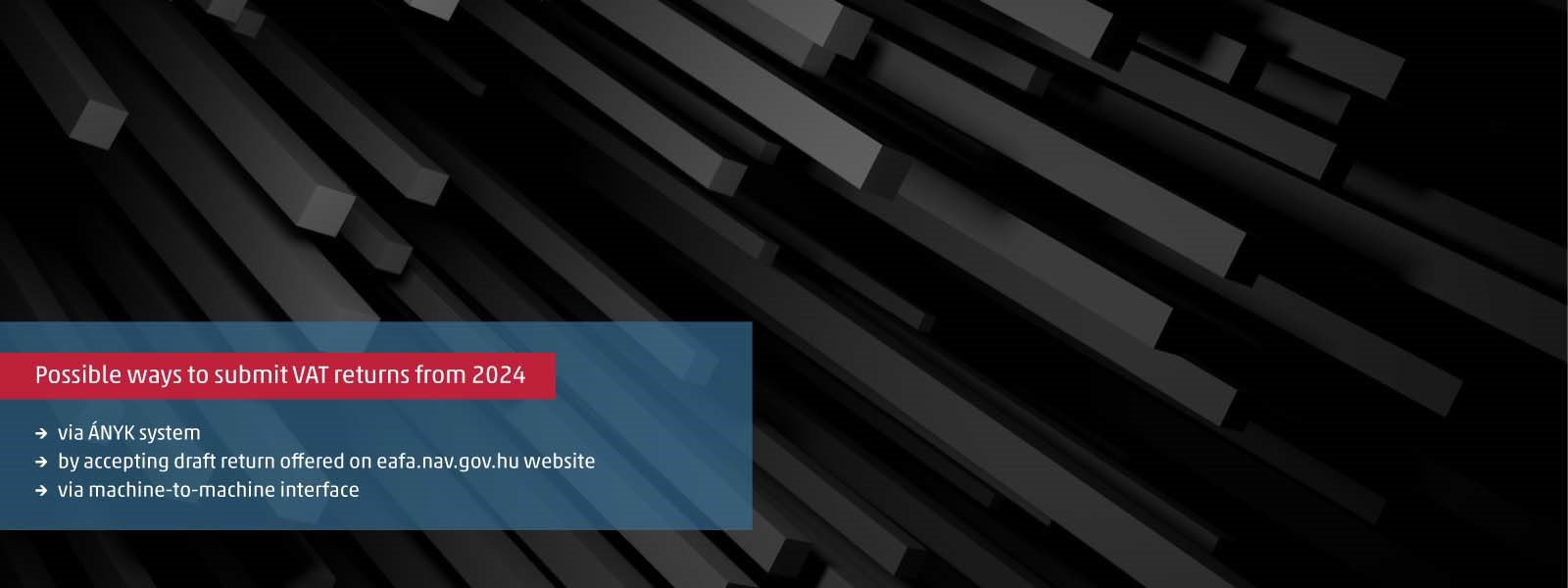

Hungarian VAT returns can be submitted in three ways from 1 January 2024. It is still possible to prepare form 65 and submit it electronically using the ÁNYK system. However, the January 2024 VAT return can already be submitted via the e-VAT system. Taxpayers have two options here: one is to accept the draft return offered on the eafa.nav.gov.hu website, the other is to accept the draft return based on return data submitted to the NAV via a machine-to-machine interface.

For traditionally filed returns, the so-called form M (detailing domestic purchases and sales by partner and by invoice) and form K (detailing adjustments to domestic purchases and sales invoices) must be completed, and preparing them – or checking if prepared using automated tools – can mean significant additional administration in the event of large-volume transactions. The tax authority does not validate the data submitted; if it finds any discrepancies, it initiates a data reconciliation or possibly a compliance investigation, which may lead to penalties.

If the draft return is approved on the website, the data available to the NAV must first be supplemented (e.g. with incoming EU items), and a declaration must be made on exercising the right of deduction and its scope. As with the online invoicing interface, the return can be accessed by the primary user (company’s legal representative or permanent authorised representative). It is also possible to set up secondary users, who can modify or supplement data, but only the primary user has approval rights. Validation is obviously not necessary in this case, as the data available to the NAV forms the basis of the return, so there is no need to prepare and submit forms M and K.

If the VAT return is submitted via the machine-to-machine interface, the data has to occur in the manner and with the data structure published by the tax authority. In this case, the taxpayer sends the NAV the document-level data underlying the assessment of tax payable and the right to deduct tax, essentially converting its own VAT sub-ledger into the data structure required by the NAV, and forwarding it. There is no need to submit forms M or K in this case either. Draft returns thus prepared must be approved by the taxpayer using automated means. The big advantage of this procedure is that, once submitted, the tax authority validates the data (compares it with the data it has) and sends information on the result of the validation (i.e. signalling any discrepancies). Using this option is subject to notification and requires some prior development.

Unlike the e-PIT system, it is important to know that for the e-VAT system (website and machine-to-machine connection) the returns submitted here are not automatically accepted, they must always be approved.

Other benefits of e-VAT system

The NAV uses the data on the online invoice, from the online cash register and from the import VAT systems to prepare the draft. Printed tax returns can only be subject to self-revisions on paper, while self-revisions of e-VAT returns can be handled both on paper and electronically. If a return is submitted in more than one way, the first submitted return is considered the one filed.

Just like e-invoicing is for VAT digitalisation, the use of e-VAT is not currently mandatory either, but the benefits make it worth exploring the possibility of applying it, and possibly rethinking the process of filing, digitalising and automating returns.

VAT digitalisation tools are not just a weapon for tax authorities in the fight against tax evaders, they can also provide taxpayers with numerous benefits, simpler administration and cost savings. They allow for automation too, but it is important to know that the system cannot replace expertise and some of the decisions that need to be made, so accountants and tax advisers will still be needed to check the accuracy of VAT data. The tax advisers of WTS Klient Hungary will gladly assist you with their up-to-date knowledge and professional experience.